A new rule allows businesses to claim a significant tax deduction for the construction or expansion of qualifying manufacturing and agricultural production facilities.[1] This new rule allows a business to claim 100% depreciation in a single year, rather than spreading depreciation over the life of the asset. Deployed properly, this accelerated depreciation can quickly reclaim a significant amount of money invested in the project.

Businesses can claim the deduction starting with tax year 2025. However, the IRS has only issued temporary guidance while it finalizes the necessary regulations, and many of the rules are subject to change.[2]

The rest of this blog post can help you identify whether your business may qualify for accelerated depreciation under this IRS’s initial guidance. If you believe you have a qualifying project, a Critchfield attorney can help you verify eligibility, claim the deduction, and ensure your business complies with all the rules and requirements.

What Property Qualifies?

For a business to claim this deduction, the property must be:

- Within the United States or its territories;

- Non-residential;

- Used for “qualified production activity;”

- Constructed, owned, and used by the same entity (i.e. no leasing);

- Constructed between January 19, 2025 and January 1, 2029; and

- “Placed in service” (i.e. complete and ready for use) between July 4, 2025 and January 1, 2031.

Two additional considerations when deciding whether to claim the deduction are:

- Partial Qualification – If only portion of a project qualifies, you may still be able to claim the deduction for the qualifying portion of the property.

- Continuing Qualification – The property must continue to remain qualified for at least 10 years after a business claims the deduction. If the property ceases to be qualified during that time, the IRS can recapture the tax savings and other negative legal or tax consequences may follow.

What is “Qualified Production Activity?”

“Qualified production activity” broadly covers most activity involved in the process of creating a product – so long as that the product is not consumed by purchasers on site (i.e., restaurants and bars are excluded). The three primary categories are:

- Agricultural Production – Including preparation, feeding, cultivation, harvesting, breeding, or managing crops and/or livestock.

- Manufacturing – Including the creation of parts, components, or complete products, as well as certain refining and processing activities.

- Chemical Production – Including preparation of raw materials, combination or synthesis of materials, isolation of materials from byproducts, and purifying materials.

The activity must directly involve the creation of the product. This generally excludes supporting and administrative activities and structures such as offices, administrative services, lodging, parking, sales, and research, development, or engineering. However, certain supporting structures like warehouse space and loading bays can qualify if they are sufficiently integrated into the production process.

A Critchfield attorney can help you determine whether part or all of a project may qualify. Claims for non-qualifying projects can lead to negative tax and legal consequences. At this time, the IRS has proposed various tests for different types of “qualified production activity.” However, these tests may change as the IRS finalizes implementing regulations.

How Does Accelerated Depreciation Work?

The new rule functions by allowing you to “accelerate depreciation.” The result is that you can claim a single, large tax deduction all at once, rather than having to claim many smaller deductions over ten years or more.

Accelerated depreciation can free up additional cash and allows your business to immediately begin recouping the cost of construction and reinvest that money elsewhere. Additionally, this deduction does not have a maximum cap or limit. This lack of a cap may allow you to claim an overall net operating loss for tax purposes. This can significantly reduce your tax burden for the year and creates a deduction that can partially be carried over to later years.[3]

The rest of this section provides a brief overview of how both standard and accelerated depreciation function.[4]

Standard Depreciation

Most property that isn’t land loses value over time as it breaks down, gets used up, or becomes obsolete. This is most commonly true for things like tools, equipment, and vehicles, but can also apply to buildings and other structures. This gradual loss of value is called “depreciation.”

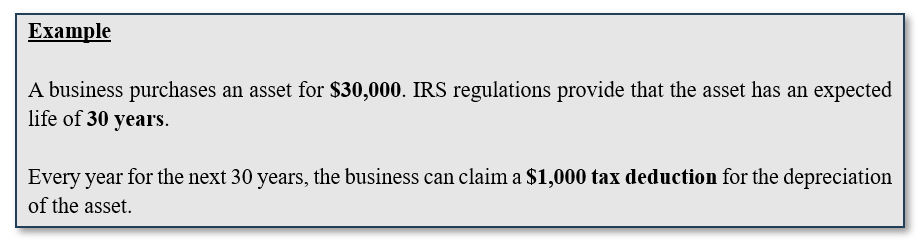

Businesses can claim a tax deduction for the depreciation of certain business property. A taxpayer must typically claim this deduction over time as a property actually ages. While there are different calculation methods, each year’s deduction is typically determined by taking the original cost of the property and dividing it by the IRS’s estimated “useful life” of the property.[5]

Depreciation generally provides positive tax benefits. However, if a business sells a depreciated asset for more than its supposedly reduced value, the IRS may be able to “recapture” some or all of the depreciation claimed in previous years.[6]

Accelerated Depreciation

Accelerated deduction simply allows a business to claim a large amount of depreciation all at once instead of over time. (In this case, 100% of the total allowable depreciation.)

In the example above, that means the business can claim a single $30,000 deduction in the first year, rather than having to claim an annual $1,000 deduction for the next 30 years.

As with standard depreciation, the IRS can potentially “recapture” depreciation if and when the property is sold. Accelerated depreciation means that the entire sales price of the property is considered taxable gain. Depending on the circumstances, this may make accelerated depreciation the wrong choice if the business plans to sell the property in the near future.

For businesses planning or currently working on new construction, the new rules for accelerated depreciation can offer immediate benefits that support long-term growth. To take full advantage of this opportunity, you should coordinate closely with tax and legal professionals.

Critchfield can help you maximize your results while reducing risks and ensuring your business remains compliant with the newest rules and developments. Follow us here or on social media to keep up with the most important changes and announcements for this and other tax incentives.

[1] IRC 168(n), introduced as part of H.Con.Res.14 – 119th Congress (2025-2026).

[3] See generally IRC 172 for the basic rules regarding the net operating loss deduction

[4] See generally IRC 167 and IRS Publication 946 for more detailed information on how the depreciation deduction functions.

[5] This is the “straight line method” of calculating depreciation. While certain types of property can use other methods of calculation, the straight line method is the simplest and most common.

[6] The rules regarding property “basis” and the calculation of gains and losses are beyond the scope of this post. However, these are things that you and your tax advisor will want to consider when deciding whether to claim accelerated depreciation.

Tagged In:ConstructionCorporate and Business